Intel Theories

We rounded up everyone's take on the US government's deal with Intel

On Friday, the Trump administration and Intel announced that the company’s Chips Act grants will be exchanged for a 10% government equity stake in Intel. We collected everyone’s takes on the deal — some previously published, and some exclusive to our Substack. 👇

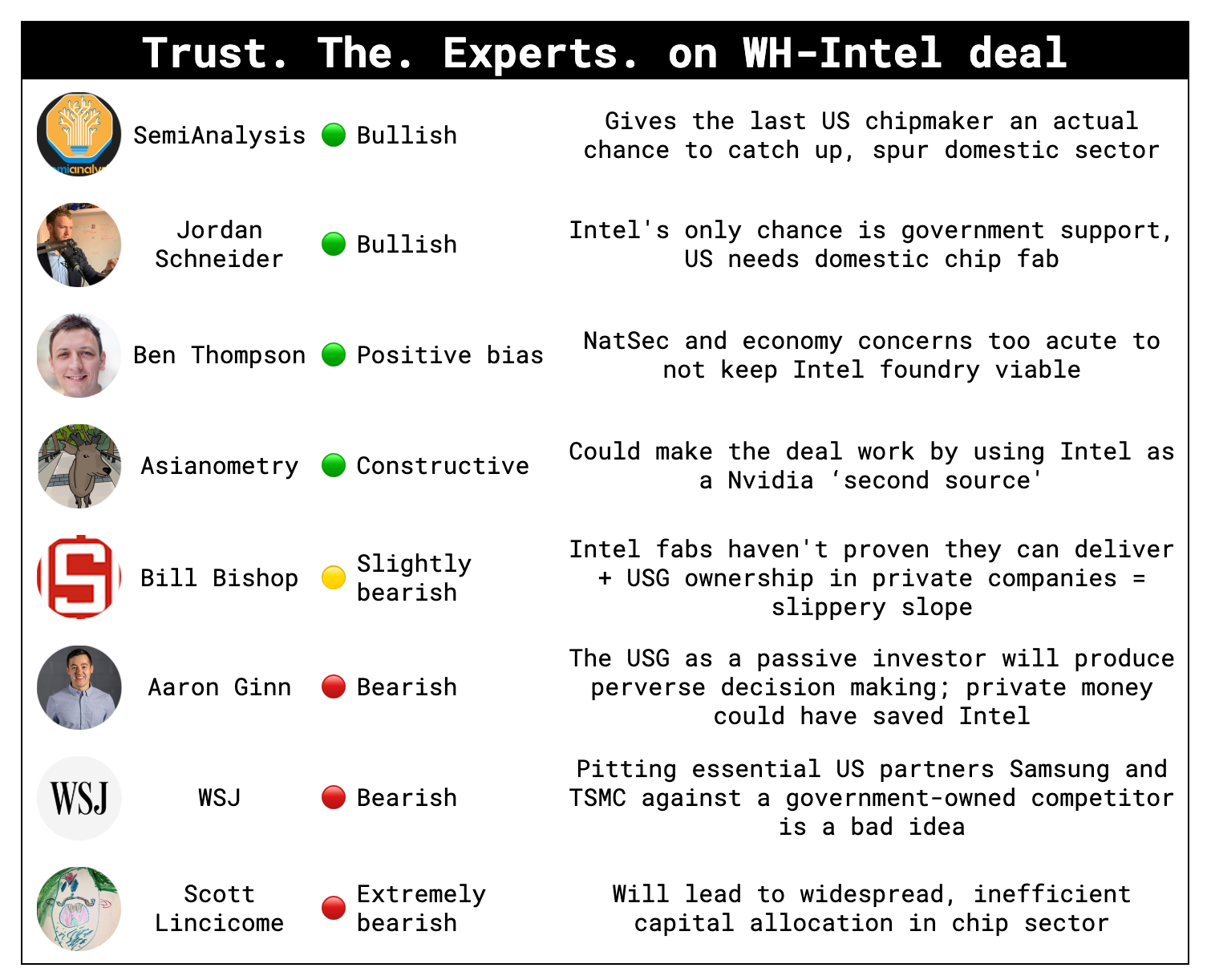

SemiAnalysis: bullish

With a stake in Intel, SemiAnalysis (and President Doug O’Laughlin) believes the government will use political leverage and tariffs to pressure companies to buy from Intel (Intel’s biggest problem being that they can’t get customers). Given that Intel is America’s last and only option for domestic chipmaking, the investment will put the company in a position to fix its foundry process, thus ultimately on-shoring critical supply chains. From SemiAnalysis on X:

“The USG investment in Intel is historic and unprecedented, but it is the first important step in the right direction. Intel is the ONLY domestic option, and today’s partnership should hopefully kickstart one of the hardest issues Intel has had: attracting customers.

“Orders and investments in Intel from the industry are now not subject to tariffs, and are investments in US manufacturing. By taking a leadership stake, now it is clear how we make chips in the US again, and that is at Intel.”

And from SemiAnalysis President Doug O’Laughlin:

“Intel’s ‘chicken-and-egg problem’ is solved. Their process is mediocre and customers don’t like it, so it can’t win customers. Now, Trump has forced them to have customers, and the foundry process could finally be fixed via forced partnership. In my view, this is an obvious path and probably one that is very good for Intel, America, and US foundry customers. I really like the partnership and think that it’s a win-win for everyone.”

Jordan Schneider at ChinaTalk: bullish

We spoke directly with Jordan. Here’s what he said:

“Intel will only make it through with government support, and the only way to get Trump to care is to give 'him' a piece of the upside. Now they just need to keep him interested long enough to get him to browbeat them some real customers.”

Ben Thompson at Stratechery: constructive/ positive bias

Ben has reservations about the government’s new equity stake, but considers the government’s play here the least bad option, mostly on the macro argument that a US with no plausible way to manufacture its own chips is intolerably risky, even if its allies manufacture them. Just as important, Thompson argues, is that the government’s position in the company guarantees Foundry’s continued existence, which the company needs to attract would-be customers, and which — again — on-shore critical supply chains. He wrote:

“Intel needs an external customer to make its foundry viable, but no external customer will go with Intel if there is a possibility that Intel Foundry will not be viable. In other words, the stakes have changed from even earlier this year: Intel doesn’t just need demand, it needs to be able to credibly guarantee would-be customers that it is in manufacturing for the long haul. […]

“The problem [with relying on allied countries for manufacturing is that it pins] all of the country’s long-term chip fabrication hopes on TSMC and Samsung not just building fabs in the United States, but also building up a credible organization in the U.S. that could withstand the loss of their headquarters and engineering knowhow in their home countries. There have been some important steps in this regard, but at the end of the day it seems reckless for the U.S. to place both its national security and its entire economy in the hands of foreign countries next door to China, allies or not.

“Given all of this, acquiring 10% of Intel, terrible though it may be for all of the reasons Lincicome articulates — and I haven’t even touched on the legality of this move — is I think the least bad option.”

Jon at Asianometry: Constructive

While Jon at Asianometry didn’t offer direct critiques or praise of the deal in his most recent video on the subject, he did offer a recommendation for how Intel could kickstart its new relationship with the US government: become a second source for Nvidia compatible chips. Basically, Jon sees the government putting up money for Intel to finish its fab in Ohio, then raising tariffs on non-domestic chips, then applying pressure on tech giants to throw some orders at Intel foundry. From here, Jon gets to his plan:

"Nvidia issues Intel a license for the patents and IPs in the Nvidia CUDA and AI ecosystem... with the goal being that Intel can produce Nvidia compatible chips in their American fabs, to be sold as a second source... Intel could issue an x86 license [to Nvidia] in return.

"[This] allows Intel to develop an in-demand leading edge product, but do it in the way that they are familiar with — by working closely with their folks at manufacturing. And Intel manufacturing can get comfortable with its internal customer on a technically demanding high volume product to clear the pipes and get its kitchen ready for opening to outside customers (no dealing with seven very mean tech giant customers).”

Aaron Ginn: bearish

We spoke directly with Aaron. Here’s what he said:

“I don’t really like it. A few reasons:

The US government has picked a de facto winner, which means no other entrants for the time being.

The US couldn’t find any other investors, so they clearly had to step in.

That said, this is a national security concern, so I am empathetic to the decision. I predicted it several months ago.

Intel’s problems extend beyond the last few years. It was decades in the making.

The US government interferes with companies regularly. That isn’t abnormal, and firms can still effectively function. Subsidies and grants are common in key critical industries. But I would have preferred a tax credit to make chips domestically over nationalization.

The US government is unlikely to be a passive investor, and has a long history of perverse decision making when in these positions.

I think someone would have filled the market hole if Intel went under, but no one offered because the market saw that the government was planning to intervene. This is just like other tragedy of the commons, or public money pricing out private money instances.

I suspect this ownership is short term, and will be sold in a couple of years.

I also predict more pressure to move business away from TSMC.”

Bill Bishop, author of Sinocism: slightly bearish

We spoke directly with Bill. Here’s what he said:

“One of the China-focused chat groups I’m in is joking about how Trump team — especially Lutnick — is going to set up a US version of China's SASAC (State-Owned Assets Supervision and Administration Commission), the body that oversees the 100+ centrally owned state-owned enterprises.

“Seriously, the deal should remove any administration doubts about Lip-Bu Tan’s ‘loyalty,’ but it is not at all clear how it fixes Intel's myriad operational and execution issues. Maybe the US will ‘encourage’ US companies to fab chips at Intel, but that only works if the fabs can deliver, and so far they cannot. I hope it works, but it is slippery slope if the Trump Admin wants to build a portfolio of state-invested companies.”

Writing for the WSJ: Mike Schmidt and Todd Fisher: bearish

In a WSJ op-ed titled ‘Uncle Sam Shouldn’t Own Intel Stock,’ Schmidt and Fisher argue that the Chips Act was designed to boost U.S. semiconductor manufacturing for national security, not to generate government profits — and it’s already paying off, with more than $500 billion in new investment announced. Intel’s real problem is its foundry, which lacks external customers, not capital. Turning grants into equity will raise Intel’s costs, distort the market, and politicize U.S. chip strategy just as America is regaining its footing. From the piece:

“The taxpayer’s return on these investments comes not in the form of revenue for the government but enhanced national security and supply-chain resilience. Turning Intel’s grants into equity would weaken U.S. competitiveness and introduce unnecessary and novel policy risks related to government ownership in the economy.”

Scott Lincicome, VP general economics and trade at Cato Institute: extremely bearish

Lincicome argued in the Washington Post that the deal is really bad, for several reasons. It will incentivize Intel’s decisions moving forward to be politically motivated, rather than to the benefit of shareholders; “a layer of political oversight” will add yet more friction to an already struggling business; other tech companies will be incentivized to buy subpar products from Intel to avoid being targeted by the White House; the admin could withhold tariff relief or export licenses from firms unless they buy from Intel. More generally:

“…America’s technological leadership emerged not from government direction but from competitive markets rewarding innovation and punishing corporate mistakes and inefficiency. If national security demands Washington support U.S. chipmakers, many policies — market and non-market — can achieve that objective while avoiding the risks raised by the Intel equity stake.”

Maybe I misread intels sec filings on the matter. Or maybe they have changed. But based on my readings and a confirmation from ChatGPT , the dept of commerce got warrants for intel stock that can only be exercised if intel sell 50 pct of its foundry.

In that event they can get intel shares.

If within 5 yrs , intel does not , the dept of commerce gets nothing.

In all cases Intel gets all its promised chips act money if they live up to that agreement.

Anyone else read it differently